Can a person just file bankruptcy on medical debts? Read our latest blog post on Medical Bankruptcy.

Can a person just file bankruptcy on medical debts? Read our latest blog post on Medical Bankruptcy.

“I want to file medical bankruptcy.” I get that phone call a lot. The situation is that many people are current on their house, car and credit card payments, but they were hit by a wave of medical bills and just want to file bankruptcy on those debts. Can a person just file bankruptcy on medical debts? Is there such a thing as medical bankruptcy?

Technically, there is no such thing in the law as medical bankruptcy, and there is no way to file bankruptcy by only listing medical debts. When you file bankruptcy all debts are listed. In fact, when somebody files bankruptcy they sign a sworn statement that says, under penalties of perjury, that they have listed ALL their debts.

When someone says they filed medical bankruptcy what they mean is that they filed not because of irresponsible spending but because of something beyond their ability to control–their health. You hear the term medical bankruptcy a lot for good reason.

NerdWallet estimates for 2013:

“Medical Bankruptcy” is really Chapter 7 or Chapter 13 Bankruptcy.

When someone says they filed medical bankruptcy they really mean to say they filed Chapter 7 or Chapter 13 bankruptcy. All debts must be listed, even the ones you want to keep, such as auto and mortgage debts. However, this is not really a big problem you can sign Reaffirmation Agreement in Chapter 7 cases to keep and revive the debts you want to keep. A Reaffirmation Agreement basically pulls a debt out of the bankruptcy case so that you can keep the car, home, etc, and continue the benefit of getting positive credit reporting.

Ongoing Medical Bills: The benefit of Chapter 13 cases.

I meet many clients who suffer from ongoing medical problems. Even if they file Chapter 7 today to wipe out the medical bills, in six months they are right back where the started with new medical debts. They may lack health insurance or the insurance they have contains loopholes that don’t cover certain medical treatments. Such individuals may benefit from the extended protection of Chapter 13. Chapter 13 cases can be open from 3 to 5 years and may eventually be converted to Chapter 7 to add new medical bills that accrued during the bankruptcy. While a person is in Chapter 13 creditors may not garnish paychecks or bank accounts. In some ways, Chapter 13 is something of a drastic form of health insurance.

Image courtesy of Flickr and Scott Kless.

Believe it or not, a good bankruptcy attorney can show you how to avoid filing bankruptcy when you visit them before it is too late.

A recent client asked this great question:

Is there such a thing as getting help to avoid bankruptcy? My wife and I have a small business. We are struggling to keep it going. We’re down over 50% this year, we’ve cut some expenses, and customer payments are dragging. While we are not unique, and I am sure you have heard it before, but we would like to avoid drowning. Please let us know if you would be available/interested in a consult.

The short answer is YES! We help people avoid bankruptcy every day. Filing bankruptcy is something you do when nothing else works. It is the last option. The process of deciding to file bankruptcy is really a process of elimination–when no other option solves the entire debt problem you then focus on bankruptcy. Partial solutions are no help. Settling one debt or one lawsuit is nice, but if it does not solve the whole problem it is just throwing money away. The benefit of bankruptcy is that it is a complete solution.

So how do we help clients avoid bankruptcy?

DEBT PAYMENT PLANS.

How much does it cost per month to get out of debt? You must answer that question before you consider bankruptcy. This is a two-step process:

STEP ONE: List the debts. Making a list of your debts is about as much fun as getting on a scale after going out for dinner. There comes a time when you stop opening the mail and lose track of how much you owe. It’s depressing so you avoid it. If you really want to avoid bankruptcy you need to write down a list of who you. Follow these steps to prepare a list.

STEP TWO:

DEBT SETTLEMENT.

Most of the people in debt settlement programs should not be in them. Most of the debt settlement plans I review have virtually no chance of succeeding. Why? You need money on hand to settle debts. If you cannot raise enough settlement funds quickly enough the creditors will file lawsuits and begin garnishments before you can settle all the debts. As a general rule, you need about one-third of what you owe in cash within 6 months of stopping payments to creditors to have any chance of settling all the debts. Creditors will typically settle debts for about 40% of what is owed, but they want the settlement in cash now. If you are able to raise cash quickly debt settlement might be an option. We help clients settle credit cards and other debts every day, but only if we see a reasonable chance of all accounts being settled.

LAWSUIT DEFENSE.

Can the creditor prove you owe the debt? Has the Statute of of Limitations expired? Can the creditor provide a copy of the credit card agreement? Are you being sued for a medical debt that your health insurance should have covered? Over 90% of creditor lawsuits result in Default Judgments. We can show you how to respond to lawsuits and to demand an accurate accounting of the debt.

BUSINESS REORGANIZATION.

Sometimes a small business is so overcome by debt that it must reorganize. Some small business corporations are so saturated with debt that it must start over. It is possible to form a new corporation and start with a clean slate. There are special rules to follow to prevent the old corporation from contaminating the new company, but this is a valid strategy to reorganize without filing bankruptcy. Personal guarantees of business debts must be considered as well.

The bottom line is, there are many ways out of debt. You need to consult with an attorney that carefully goes through each option. That is what we do. We can help you avoid filing bankruptcy if you visit with us before the situation gets out of hand.

Image courtesy of Flickr and David J. Dalley.

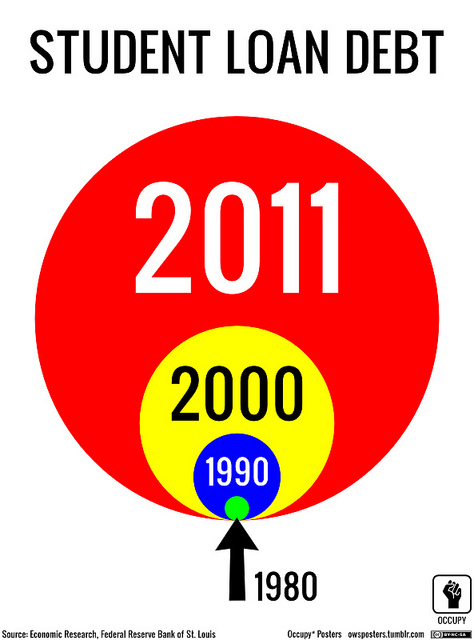

I’m seeing a lot of new lawsuits filed by the National Collegiate Student Loan Trust for unpaid private student loans. Check out our most recent post on how to respond to these lawsuits in Nebraska.

Private Student Loans are the single worst debt in existence. They lack any formal Income Based Repayment (“IBR”) plans and the debts are generally not discharged in bankruptcy without undergoing expensive litigation and claiming a special hardship. In recent years, the National Collegiate Student Loan Trust, the largest holder of private student loans, has filed thousands of lawsuits against delinquent borrowers, and I count several hundred such lawsuits filed in Nebraska.

National Collegiate lawsuits are really no different than a basic credit card case, and they suffer many of the same problems:

Trusts Lack Capacity to Sue in Nebraska.

As a general rule, a trust is not a legal entity and lacks the ability to sue or be sued. Rather, the lawsuit should be brought in the name of the Trustee. (See Black Acres Pure Trust v. Fahnlander, 233 Neb. 28 (1989)). The Uniform Law Commission has written extensively on this issue and has proposed a uniform law to create “statutory trusts” that would enjoy the same rights given to corporations to sue or be sued.

A common-law trust arises from a private action without the involvement of a public official. Because a common-law trust is not a juridical entity, it must sue, be sued, and transact in the name of the trustee and in the trustee’s capacity as such. By contrast, a statutory trust is a juridical entity, separate from its trustees and beneficial owners. It has the capacity to sue, be sued and transact on its own.” Uniform Law Commission.

So, is National Collegiate a “common-law” trust or a “statutory” trust? Does that distinction make a difference in Nebraska? National Collegiate is organized as a Delaware trust agreement and that state does provide for statutory trusts empowered to sue. There are arguments to be made both ways, but until the courts rule on this issue, the first defense to these lawsuits is to file a motion to dismiss.

National Collegiate Must Show They Own the Loan.

You did not borrow money from National Collegiate. Most likely the loan originated from JPMorgan Chase or Bank of American or Charter West Bank. The loan was then assigned several times and eventually wound up in one of the several trust pools managed by National Collegiate. It is essential that National Collegiate be required to provide the “chain of assignment” showing how your loan was specifically assigned from the original lender to the National Collegiate Trust. Failure to prove the entire chain of assignment means the lawsuit must be dismissed for lack of standing.

Statute of Limitations.

In Nebraska, lawsuits filed for breach of a written promissory note must be filed within five (5) years of the date of last payment or from an acknowledgement of the debt. It is important to demand an account payment history from National Collegiate to verify the date of last payment. Very often the records of National Collegiate are sketchy at best and they seem to struggle to provide detailed account statements. If they do assert a payment was made in the preceding 5 years, research your bank statements to see if their record of payment matches your records.

Did a Prior Bankruptcy Case Discharge Some of the Student Loan?

Have you filed bankruptcy before? If so you may have discharged some of the National Collegiate obligation already. Although Federal Student Loans are not discharged in bankruptcy (unless you receive a Hardship Discharge), when it comes to Private Student Loans only the amount qualified under Section 221(d)(1) of the Internal Revenue Code is excepted from discharge. I have seen cases where loans were made for $30,000 per year when the actual cost of attending the college, including tuition, books, room and board and transportation expenses, was only $10,000 per year. Also, only loans to a qualified educational institution are protected. National Collegiate often sues for debts that have been partially or entirely discharged.

Statute of Limitations are not Tolled During a Chapter 13 Case in Nebraska.

If you can go five years without making a payment or requesting a loan deferment, the Nebraska statute of limitations may apply. (See National Bank of Commerce v Ham, 256 Neb. 679 (1999))., The 5 year limit must run prior to the commencement of the lawsuit and you must affirmative claim this defense in the written answer filed with the court. If you sense that you are about to be sued by National Collegiate, consider filing Chapter 13 to run out the SOL clock.

Negotiate the Debt.

National Collegiate is willing to cut a deal. Even if they are successful in obtaining a judgment, they still have the burden of collecting the debt. The fact that they have initiated a lawsuit means that they probably have not received any payment in years. I have represented clients who were able to settle $150,000 of loans for $30,000. Each case is unique, but National Collegiate is willing to consider reasonable settlement offers.

Image courtesy of Flickr and Occupy* Posters.

It seems like a lot of people are shocked to learn that they have been sued or that judgments have been registered against them. I remember speaking to a new client recently and it was unclear how much she owed and from what she was saying her total debts were less than $5,000, an amount clearly not worth filing bankruptcy over. While we were talking I checked the Nebraska court’s online records to see if any judgments were filed against her, and to her great surprise a $30,000 judgment lien had been filed against her residence! Needless to say, she and her hubby had a fun chat that evening.

When debt problems get bad, sometimes we stop opening the mail. People move from town to town seeking better jobs, housing or schools, and it is common for creditors to serve notice of lawsuits on former addresses. One client was shocked when I informed her a judgment had been issued against her after the Sheriff served notice on her 10-year old daughter who forgot to give her mother the paperwork when she arrived home for work. Clients commonly have no clue who they owe or if they have been sued, but they have a nagging sense they owe a lot and they need help. Figuring out who you owe and how much you owe is the first step in crafting a plan to get out of debt.

A new system developed by the Nebraska Court Administrators office allows anyone to search for lawsuits and judgments online for a small fee (currently set at $15). Here is the link to the Nebraska Justice Search system. This same information is generally available at the local county courthouse for free.

How do I pay a judgment I find online?

If you discover that you owe a judgment, there are several ways to pay it.

If a judgment has been entered against you it is important to get a Satisfaction of Judgment filed in the court record after payment. Once the judgment is paid or settled, you want the public records to show the debt is satisfied so that you may update your credit report.

Image courtesy of Flickr and lemonjenny.

As the old saying goes, if you don’t use it you lose it. The “it” in this case is the right to sue someone for an unpaid debt. Every state has a set of laws that create a deadline for creditors to sue for an unpaid debt. In Nebraska there are two key laws that govern debt collectors when it comes to suing for an unpaid debt.

In recent years there has been a dramatic increase in sale of these time-barred debts to junk debt buyers who call to collect debts that are 5, 10, 15 or even 20 years old. Very often they lack any real documentation of the debt owed and they try to trick the debtor into making a voluntary payment, thus resetting the statute of limitation. I am frequently hearing clients and former clients call about abusive phone calls where the debt collector threatens to have the debtor arrested that very day if a payment is not made.

WHAT SHOULD YOU DO IF YOU ARE SUED ON AN EXPIRED DEBT?

IS THE STATUTE OF LIMITATIONS TOLLED DURING A BANKRUPTCY CASE?

This is a very important topic for attorneys practicing in consumer bankruptcy cases who represent debtors owing Private Student Loans. Bankruptcy Code Section 108(c) provides that if a statute of limitation would normally expire during the administration of a bankruptcy case, the statute is tolled for an additional 30 days after notice of the end of the bankruptcy case. The big question is whether the Nebraska statute of limitations is tolled during the administration of the bankruptcy case. The answer to that question was provided by the Nebraska Supreme Court in the National Bank of Commerce Trust & Savings Ass’n v. Ham decision. In short, the court ruled that the Nebraska statute of limitation is not tolled during a bankruptcy case except for the additional 30 days provided under Section 108(c) of the Bankruptcy Code. This is a very key ruling for debtors owing substantial private student loan debts who may benefit by filing a Chapter 13 bankruptcy case to seek protection while the statute of limitation runs out on their private student loans. More on this topic later.

Image courtesy of Flickr and Patrick Marlone.

Can I keep my home if I file bankruptcy? Do I have to list the mortgage company? What if I’m behind on the payment? Can I still pay the mortgage payment online? Will they send me monthly statements? How do I know that the past due amounts were paid current? I want to file bankruptcy but I don’t want to lose my home. I don’t want to list that debt.

Homeowners have a lot of anxiety about filing bankruptcy, and for good reason. They worry that by filing bankruptcy they will lose the home. To be sure, there are risks to filing bankruptcy, but the whole idea of filing a case is to protect property and there is no reason a home should be lost or compromised if you observe the following:

Image courtesy of Flickr and Andrey 77 dron.

I enjoy listening to a variety of podcasts while walking the dog or driving to the office. Podcasts are a really amazing thing for those who crave learning, although there seems to be some rule that requires 50 bad shows to appear before you find a really great one. (Have you loaded the Stitcher radio app on your smartphone yet? You really should.) The EntreLeadership podcast is one of the better shows being streamed these days, and I had the pleasure of listing to Dale Partridge talk about his new book, People Over Profits.

As you might guess, the message of the book is that a business will not succeed in the long-run if it places profits over people, despite some evidence to the contrary. Perhaps it is better to say that businesses will be more successful in the long-run if they keep their customer’s best interest at heart. I think it really comes down to establishing trust. We trust that Apple computers are top notch and that Starbuck’s coffee is always great–they have earned that reputation.

What Partridge is talking about is more than just good business sense. We all need a set of core values to steer our personal lives and our businesses as well. In the long run, businesses and individuals get lost when they routinely put selfish short-term needs and wants ahead of others, especially customers.

I’d like to think we have modeled our law firm with the client needs and wants placed first. How do we do that?

Creating a customer-focused organization is expensive and challenging. It takes a lot of time and money to be responsive. In the long-run it pays off. Deciding to be great instead of mediocre takes commitment, training, planning, money, passion and dedication. I don’t want to work any other way.

Image courtesy of Flickr and Janine & Jim Eden.